Beware Trojan Horses

I’ll admit my guilt from the onset.

Even though my father left me a collection of four hundred gorgeous, leather bound and gold leafed classic books from the Franklin Mint, I’ve never even cracked the spine on most of them. Not because I’m a heathen, but because I never seem to have the time to properly enjoy and read them. These aren’t Dan Brown or John Grisham novels, but the great books of the western world. One of the many volumes in my collection is Homer’s The Odyssey.

In Homer’s The Odyssey, the Greeks famously left a wooden horse outside the gates of Troy. The Trojans, believing it a gift, wheeled it inside their fortified city. That night, Greek soldiers emerged from within and opened the gates to their army. Troy fell—not by force, but by misplaced trust. We all know the story, but admit it, you’ve never read The Odyssey either!

Today, I worry we may be witnessing a modern financial Trojan Horse being gifted to our 401k investors.

On August 7, 2025, President Trump issued a new executive order directing the Department of Labor to ease restrictions on 401(k) plans, allowing them to invest in private equity, private credit, and other alternative assets. The stated goal is to “democratize” access to investments traditionally reserved for institutional investors—public pensions, endowments, and ultra-high-net-worth individuals. On the surface, this sounds like progress. Who wouldn’t want retail investors to benefit from the same opportunities as the elite?

But as with the Trojan horse, we must ask: what’s inside?

Private equity and private credit are complex, opaque, and illiquid. They often come with high management fees, long lock-up periods, and valuation challenges. Unlike publicly traded stocks and bonds, these assets don’t offer daily liquidity nor transparent pricing on an exchange. We all like to track the prices of our investments on our smart phones and talk about the day-to-day movements. However private equities require deep expertise to evaluate and manage—expertise that most individual investors, and even many 401k and 403b plan fiduciaries, may not possess.

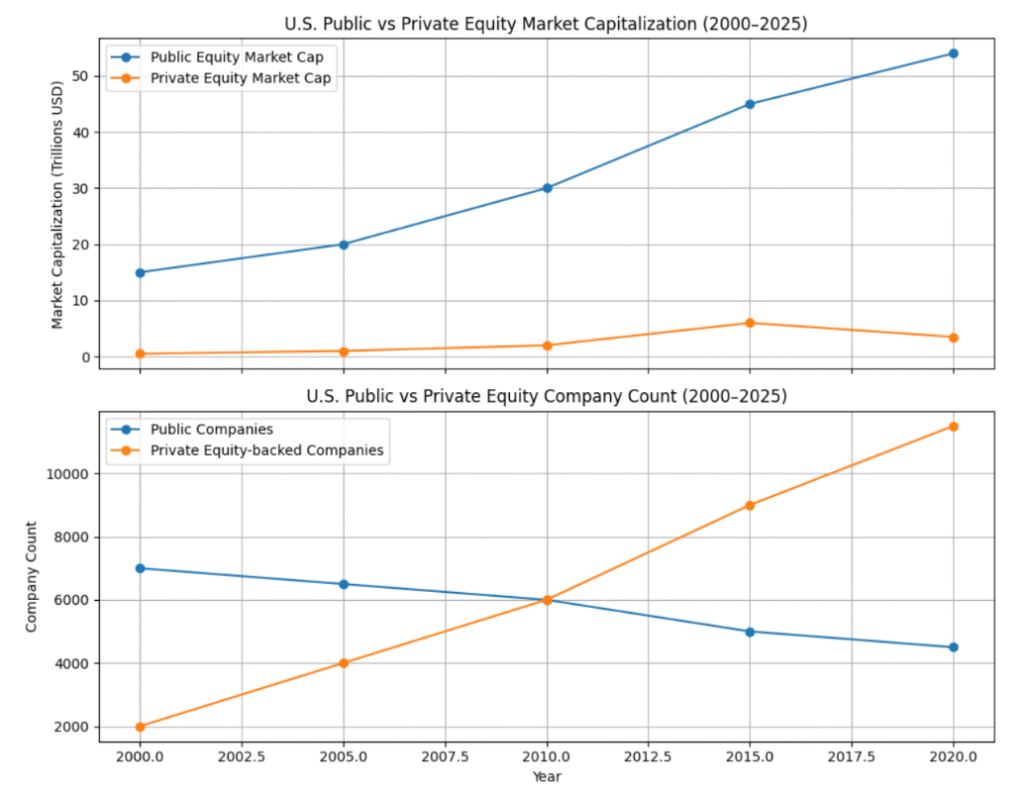

To better understand the shifting landscape, consider the chart below comparing the U.S. public and private equity markets over the past 25 years.

Two trends stand out:

1. Market Capitalization: Public equity markets have grown steadily over the past 25 years, reaching over $54 trillion in 2024. In contrast, private equity markets—while expanding—remain a fraction of that size, peaking at around $6 trillion before contracting to $3.5 trillion. This disparity underscores the relative scale and liquidity of public markets versus private ones.

2. Company Count: The number of publicly listed companies has declined from 7,000 in 2000 to around 4,500 today. Meanwhile, private equity-backed companies have surged from 2,000 to over 11,500. This shift reflects a growing preference among businesses to stay private longer, often due to regulatory burdens from the SEC and encouraged by the availability of private capital investment from institutions.

While private markets are expanding in breadth, they still lack the transparency, liquidity, and regulatory oversight of U.S. equities traded in the public markets on an exchange like the NYSE

or NASDAQ. Embedding these assets into retirement plans may expose investors to risks they do not fully understand—especially when the underlying investments are hard to value and often very difficult to exit.

Wall Street knows this. And yet, major investment firms are racing to design products that package these assets into collective investment trusts and target-date funds for 401(k) investment menus. Why now?

The answer may lie in what’s happening behind the scenes. Institutions like Harvard and Yale and other traditional PE investors are quietly offloading billions in private equity stakes. Faced with liquidity crunches and a sluggish exit environment, they’re selling their PE holdings at discounts. At the same time, Wall Street is pushing to “democratize” access—creating a new pool of buyers from the $12 trillion in 401k assets just as the old guard is heading for the exits.

This is not generosity. It’s a strategy.

When the IPO window closes and valuations falter, private equity firms need a new outlet for their own liquidity exit strategies. Retail clients’ retirement accounts—large, sticky, and less sophisticated—are an ideal target. By embedding illiquid assets into funds financially engineered for 401k’s, Wall Street can sidestep regulatory scrutiny and shift risk to everyday investors. It’s a clever move. But it’s not necessarily in your best interest.

Think about it this way; at the present moment 401k plans have not ever been able to even buy individual public stocks, ETFs and bonds (with small very small exceptions by some plan sponsors). But now the Government is okay with these same plans buying illiquid private securities? I sense the seeds for another financial crisis and Government bailout.

As your financial advisor, I believe in transparency, liquidity, and alignment. I believe that retirement savings should be built on a foundation of simplicity and resilience—not complexity and opacity. While private markets can offer attractive returns, they also carry significant risks such as the inability to sell when you want to and high management fees from these fund sponsors eating into your returns. These risks are magnified when access is granted without adequate education, oversight, or safeguards. And as a fiduciary, my first responsibility is to protect what is in my client’s best interests.

Remember, the Trojan Horse didn’t look dangerous. It looked like a gift.

So, as these new investment options begin to appear in your retirement plans at work, I urge caution. Ask questions. Demand clarity. And remember, not every “opportunity” is what it seems.

We will continue to monitor these developments closely and advocate for your interests. If you have questions about your 401k plan or want to discuss how these changes might affect your current household portfolio, please reach out.

Thank you for your continued trust.

Written by Jim Claire